The Number One Shift for Stocks This Year

Things may not be as they appear for stocks...

Before we get started, I want to welcome the +173 subscribers who signed up for the Let’s Analyze newsletter in the last week! If you want to join our community, make sure to sign up here:

The Federal Reserve just tipped their hand.

At their latest policy meeting, the US central bank said interest rate increases are nearly finished.

That means we’re close to the Fed “pivot” – or lowering of interest rates – investors have been waiting for.

At the same time, the Fed has created nearly half a trillion in cash out of thin air to rescue the US banking system. This has effectively restarted quantitative easing (QE) - or “money printer go brrr” - by expanding the central bank’s balance sheet to levels not seen in over a year…

…wiping out the a year’s worth of “quantitative tightening” in two weeks.

This combination of a looming Fed pivot and return of quantitative easing is a key reason everything from stocks to bonds to crypto are rallying.

But while I am pleased to see the Fed nearing the end of their rate hike cycle, history shows the Fed coming to the rescue with lower rates and QE is a short-term death knell for stocks.

Setting the Financial Stage

The Federal Reserve raised interest rates at its fastest pace in history last year…

…to combat the highest inflation in 40 years.

While higher rates are good for fighting inflation, they’re bad for stocks. In fact, aggressively rising rates was the main reason the S&P 500 had one of their worst years ever in 2022:

But oddly enough, the real financial fireworks often don’t start until the Fed stops raising rates and begins lowering them.

Listening to the Futures Market

Federal Reserve chairman Jerome Powell stated at his press conference that the central bank has no plan to lower interest rates in 2023.

But the market doesn’t believe him. We know that because the futures market for the federal funds rate (FFR) – the interest rate set by the Federal Reserve – is telling us so.

The futures market allows investors to buy and sell contracts that represent a prediction of what the FFR will be at a specific point in the future. For example, an investor might buy a futures contract that says the FFR will be 2% in six months' time. If the FFR is indeed 2% in six months, the investor would make a profit on the contract.

After the latest interest rate increase by the Fed on Wednesday, the FFR is between 4.75% and 5.0%. But by December the futures market is betting the FFR will be 3.75%...

…implying over a full 1.0% in interest rate cuts by the end of the year.

And if that’s the case, history shows it’ll be bad news for stocks.

Be Careful What You Wish For

Federal Reserve rate hikes in 2022 caused the S&P 500 to have its worst annual percentage loss since the Global Financial Crisis in 2008.

And while it’s counterintuitive, when the Fed “pivots” – or begins to lower interest rates as the futures market expects – stocks usually experience even more declines.

Over the last 50 years, the S&P 500 has pulled back an average of -28.3% after the Fed announces an interest rate cut:

If this trend holes, that means the S&P 500 would fall back to levels not seen since May 2020:

While the data is damning, part of me thinks this is more correlation than causation. When the Fed “pivots” on rate hikes, it usually means there’s some severe financial stress happening so it makes sense for stocks to fall.

That said, I always hope for the best and prepare for the worst. And while history shows stocks struggle after a pivot, the opposite is true for another asset class.

I’m (Still) Making Bonds Great Again

While stocks tend to crash after a pivot, the inverse is true for US government bonds.

US government bonds are a “safe haven” asset. For instance, during the COVID-19 Crash in March 2020 when the Fed issued an emergency interest rate cut, we saw US government bonds surge in value…

Bond yields and prices move inversely to each other

…a trend we also saw in 2008 during the Global Financial Crisis when the Fed aggressively cut rates:

Bond yields and prices move inversely to each other

US government bonds rise in value when the Fed pivots because when interest rates are lowered, the yield on newly issued bonds also decreases. As a result, the older bonds with higher yields become more valuable in comparison.

This creates a demand for these older bonds, which in turn drives up their prices.

This Time is Probably Not Different

I believe the futures market when it says a pivot – or lowering of interest rates – is coming in the next few months.

And while the Fed is also expanding its balance sheet to support the banking system, I expect this trend to reverse once stress in the system subsides.

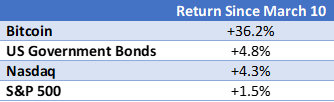

History is faily clear on how stocks and bonds perform after a pivot. That’s a key reason I’ve been selling stocks and buying bonds the last three months:

Only time will tell if history repeats itself again.

But my money is on bonds.

Stay safe out there,

Robert