My Biggest Market Call for 2023

I’m making US government bonds great again…

Before we get started, I want to welcome the +201 subscribers who signed up for the Let’s Analyze newsletter in the last week! If you want to join our community, make sure to sign up here:

Money printer go brrr – or quantitative easing – is back.

Quantitative easing or “QE” is a tool used by the Federal Reserve to stimulate the economy. It was one of the key methods used during the COVID-19 Crash in 2020 and the Global Financial Crisis in 2008 to support financial markets.

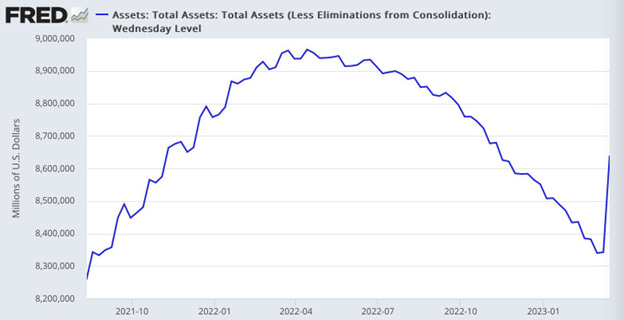

And with the Fed adding $300 billion to their balance sheet this week to counter the impact of multiple bank failures, it’s safe to say some form of QE is back…

…and that’s great news for my biggest market call of the year.

The Lender of Last Resort is Back

Stocks had a massive week last week.

The Nasdaq rose over +5% despite multiple banks failing. This only makes sense because the Federal Reserve was injecting massive amount of cash into the system via something called the Bank Term Funding Program (BTFP):

The BTFP was first introduced in March 2020 in response to the COVID-19 Pandemic. The program was designed to provide short-term funding to banks, with the goal of supporting lending to households and businesses and promoting financial stability.

But in the wake of the regional banking crisis in the US, the Fed re-started this program on March 13.

The BTFP lets banks take advances from the Fed for up to a year by pledging US government bonds and other debt as collateral. By allowing banks to pledge their bonds, they can meet customer withdrawals without having to sell their bonds at a loss.

This “forced selling” of US government bonds is what led to the bank run on Silicon Valley Bank two weeks ago.

While not identical, this program is very similar to the quantitative easing programs instituted by the Fed during previous financial crises.

A “Stealth” Quantitative Easing Program

When a central bank engages in QE, it buys large amounts of government bonds from banks. This increases the amount of money in the economy and encourages lending and spending.

That means in both QE and BTFP, the Fed is buying tons of US government bonds.

:max_bytes(150000):strip_icc()/what-is-quantitative-easing-definition-and-explanation-3305881_FINAL-68baf22f673249f4b8f43e0026c5f708.png")

I don’t see this BTFP program reversing any time soon as many banks are holding US government bond positions that are deeply in the red.

And since banks can unload these bonds and get equivalent loans in return, there is a strong incentive to keep selling these bonds to the Fed.

The Fed has nearly unlimited money. So when they buy something, the price of that good tends to rise. That’s a key reason we saw an incredible rally in US government bonds last week.

Oddly enough, it’s only one reason I’m bullish US government bonds.

US Government Bonds are Surging

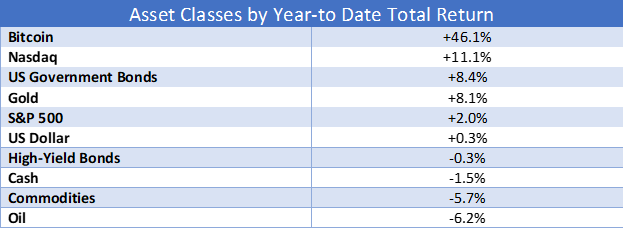

Going into 2023, one of the predictions was that US government bonds would be the best performing asset this year.

That prediction is off to a pretty good start…

…but there are a few reasons the asset class is primed for even more gains. For one, US government bond prices move inversely to the Federal Funds Rate (FFR).

The FFR is the interest rate controlled by the Federal Reserve. When people say the “Fed is raising rates” they mean the Fed is raising the FFR.

But since bond yields and bond prices move inversely to each other, it follows that a decline in the FFR means bond prices will rise.

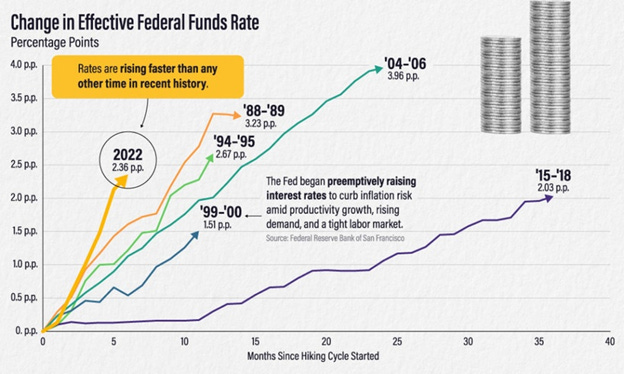

And all signs point to the FFR being at or near its peak. And while I don’t expect the Fed to cut interest rates (or lower the FFR) until the end of 2023…

the bond market is forward looking, meaning US government bond prices will move higher in anticipation of the Fed cutting rates.

But it’s not the only reason I like bonds.

The Recession (Probably) Started This Week

I’ve gone on record saying I expect a recession in 2023.

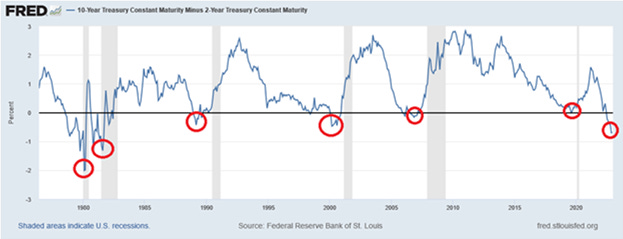

This is based on numerous factors. But the most telling is the yield curve inversion.

The yield curve inversion – or difference between the yield on the 10-year and 2-year US Treasury note – has happened before every recession since 1976:

The yield curve inverted back in April 2021. And since most inversions happen roughly nine months before recession, it follows the US will likely fall into recession in early 2023.

A recession is good for US government bond prices for a few reasons. First, bonds are “risk free” assets. When economic conditions deteriorate, investors often flock to safer assets like bonds. This in turn pushes up their prices.

But bonds also benefit when the Federal Reserve lowers interest rates. The Fed has a long history of lowering interest rates during recessions to stimulate the US economy.

And since the bond market will “front run” the Fed, we should see bond prices rise and yields fall when it’s clear a recession is near.

And there’s another key reason I’m bullish bonds.

The Inflation Story is Waning

The biggest driver of the 2022 bear market in both stocks and bonds was 40-year high inflation.

And that’s the main reason US government bonds had their worst year since the 1700s last year:

Bond prices and inflation have an inverse relationship: when inflation falls, the fixed payments that bondholders receive become more valuable. That can lead to an increase in bond prices.

And all signs point to inflation having peaked. While headline inflation is still at a high 6.0%, falling commodity, real estate, and durable goods prices imply the worst of inflation is over.

This view is already reflected in the futures market, as January 2024 CPI expectations are at 2.0%:

And since the bond market will price this in well ahead of inflation actually falling, bonds prices should rise as inflation continues its decline.

I’m Making US Government Bonds Great Again

Bonds are a foreign asset class to many individual investors.

Trust me, I know your eyes glaze over when I bring them up. But the Fed turning the printing press on via the BTFP will act as a major tailwind for the US government bond market.

We will likely get more clarity on this at Wednesday’s Federal Open Market Committee (FOMC) meeting. Right now, markets are pricing in a 0.25% basis point increase in the Federal Funds Rate (FFR).

Anything above that level will likely lead to a near-term pullback in stocks.

For now, we wait and see.

Stay safe out there,

Robert