My #1 Recession Signal is Flashing Red

The impact on stocks may surprise you…

Before we get started, I want to welcome the +101 subscribers who signed up for the Let’s Analyze newsletter in the last week! If you want to join our community, make sure to sign up here:

Sometimes it sucks to be right.

Two weeks ago, I told you the biggest risk for stocks was a resurgence in inflation.

And that’s exactly what happened; the latest Consumer Price Index (CPI) report showed inflation fell to only 6.4% instead of the expected 6.2%.

This is a key reason stocks have struggled over the last few weeks, with the Nasdaq falling -6% since the report’s release.

But markets are also in the middle of a once-in-a-decade event…

The last time this happened was in April 2007. By April 2008, the US was suffering through its worst economic slowdown since the Great Depression.

And by February 2009, the S&P 500 had cratered -44%...

…but it wasn’t the first time the “yield curve inversion” had preceded financial calamity.

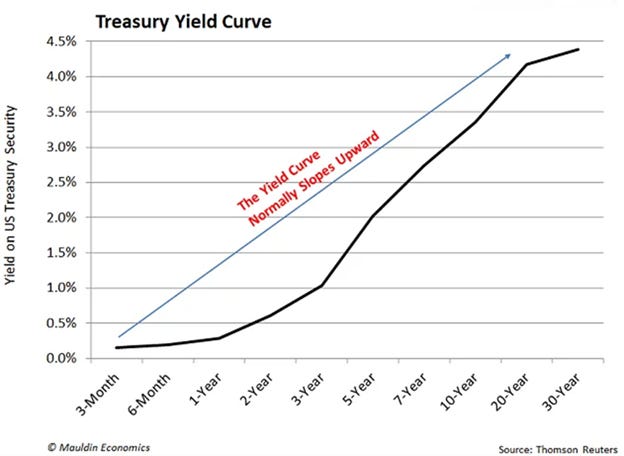

Yield Curves 101

The US government is the safest and largest lender on Earth.

Just like companies’ issue bonds to fund their businesses, the US government issues treasury bonds to finance the government.

But since the US government has never defaulted on its debt and is backed by US government assets, treasury bonds are considered 'risk-free' investments."

The US Treasury issues these bonds for different lengths of time, ranging from three months to 30 years. This period is called the bond’s “maturity.”

Normally, investors demand higher yields for longer-term bonds. This makes sense, as it’s harder to predict economic changes or major world events 30 years out.

In other words, we demand higher yields to compensate for greater uncertainty.

The longer the maturity, the higher—or steeper—the yield.

But when the yield curve inverts, the opposite dynamic plays out; investors begin demanding higher yields for shorter time horizons. This happens because investors are more nervous about the near-term (1-2 years) than the long-term (10-30 years).

And this dynamic has played out before every crisis in the last 60 years.

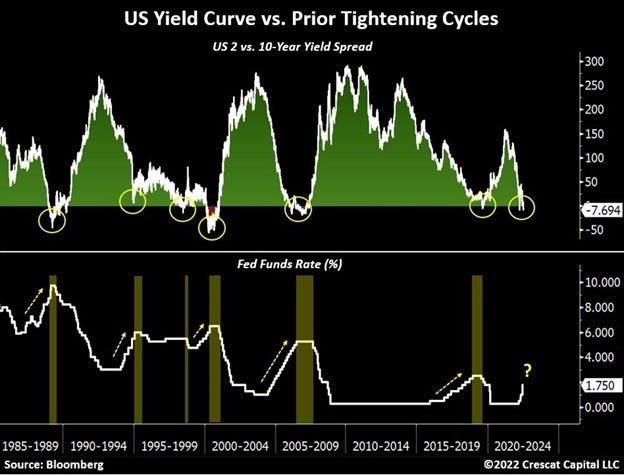

The Recession Oracle

A yield curve inversion is a sure sign that the economy is in trouble.

When investors are worried about the future, they may prefer to lend money for shorter periods of time, even if it means accepting a lower yield. This can push down long-term interest rates and cause a yield curve inversion.

And what’s interesting is this “inversion” has played out before every financial crisis since 1976…

…including the Dot Com Bubble, Global Financial Crisis, and even the COVID-19 Crash.

And not only is the curve currently inverted, but it’s also the most inverted it’s been in 20 years – even deeper than in the lead up to the Global Financial Crisis in 2008.

Only this time, the Federal Reserve isn’t going to save the market.

The Fed’s Not Coming to the Rescue

In previous yield curve inversions the Federal Reserve lowered interest rates to help juice the economy:

And the futures market expects a similar path this time around; federal funds rate futures are pricing in the US central bank to pause interest rate hikes in June 2023 and begin cutting interest rates in August 2023…

…which seems optimistic after the later CPI report came in hotter than expected.

But while an inversion is bad news for stocks over the next year, a yield curve inversion doesn’t necessarily mean stocks will struggle in the near-term.

Looking on the Bright Side…

There’s an upside to all this; a yield curve inversion is always a positive sign for stocks in the short-term.

Just look at how the S&P 500 rose after the last four inversions:

At the 18-month mark after the last three yield curve inversions, the S&P 500 had returned an average of 32%. Pretty respectable.

For perspective, that’s the same return on the S&P since May 2020…

…so not all hope is lost.

The Long-Term Picture Hasn’t Changed

There are a lot of red flags for the markets right now.

We have the yield curve inverted at its deepest level since 1980. The latest inflation report came in higher than expected. And it looks like we’re at the start of an earnings recession.

But that does not mean we’re for sure headed for a market crash. First, recessions do not always lead to stock market pullbacks. In fact, in the last 30 recessions only 14 have led to negative S&P 500 returns.

We’ve also already had a vicious pullback in financial assets, meaning the market may have already priced in a recession:

Plus, it’s important to remain a long-term optimist when it comes to investing.

So what should you do? Well, it’s a good time to hang onto some extra cash to buy assets on the cheap. My cash position is now over 26% of my portfolio, up from 12% just a few weeks ago:

I’d also “high grade” your portfolio and only hold high-quality stocks in your portfolio.

Because forecasting the market is hard. But with the yield curve so inverted, it looks like we have some economic storms brewing on the horizon.

And I intend to be prepared when it comes.

Stay safe out there,

Robert