The Biggest Risk for Stocks Right Now

The "pain trade" for stocks is lower from here…

Before we get started, I want to welcome the +639 subscribers who signed up for the Let’s Analyze newsletter in the last week! If you want to join our community, make sure to sign up here:

Stocks look vulnerable.

This may come as a surprise as the Nasdaq just had its best January since 2001, primarily because Big Tech earnings weren’t as horrible as expected.

Even though some of the world’s biggest companies reported subpar earnings (particularly Apple and Amazon), the stock market is priced on expectations. And investors expected horrible earnings, not “weak” earnings.

But that doesn’t mean the stock market is in the clear. Because on Tuesday, we’ll get important data on inflation.

The Return of 1970s Inflation

Inflation is when the prices of goods and services go up over time.

This monetary phenomenon arises when there are too many dollars chasing too few goods.

:max_bytes(150000):strip_icc()/inflation-36ec5c63655d4f2390bd5fb32cca7c75.png")

For instance, during the COVID-19 pandemic the US government gave people and businesses money to help stave of the pandemic’s economic impact. But at the same time, COVID-19 lockdowns led to supply chain issues which restricted the flow of goods in the economy.

Too many dollars (e.g. stimulus checks, PPP loans) chased too few goods (e.g. supply chain issues), which led to a general increase in prices (i.e. inflation).

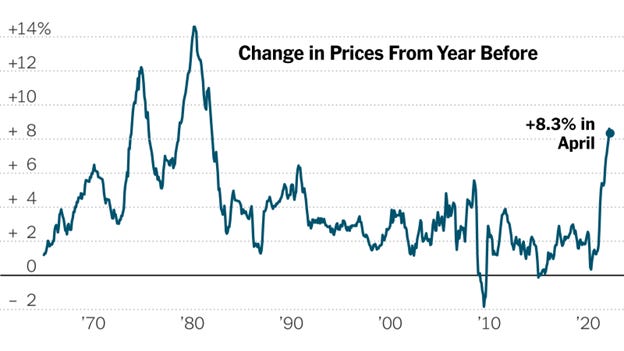

This supply and demand imbalance was so bad that the US had its highest inflation in 40 years…

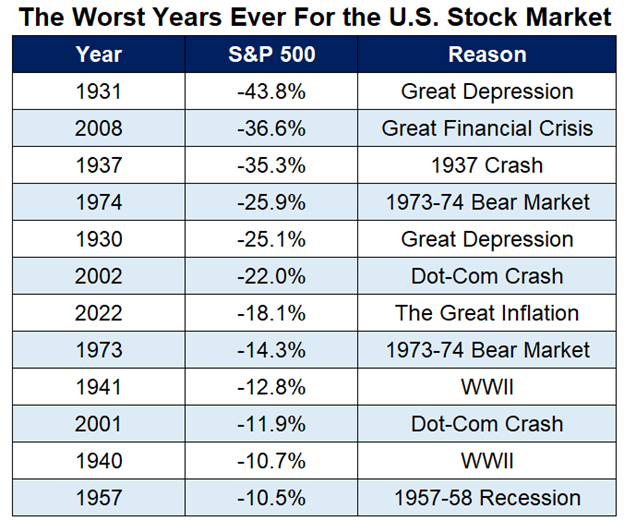

…which was the main reason the S&P 500 had its worst year since Global Financial Crisis in 2022.

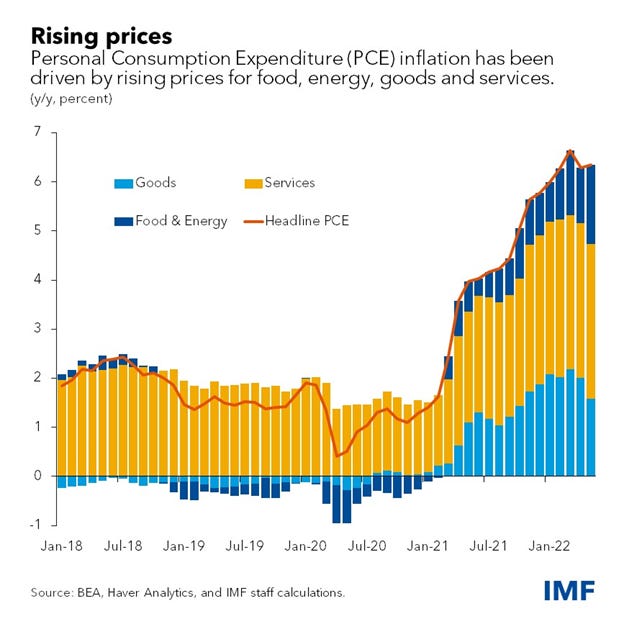

Rising Prices is Bad News for Stocks

High inflation affects businesses (and thus stock prices) in multiple ways.

When people are paying more for things they need like food, housing, and transportation, they don’t have as much money to spend on things like iPhones, video games, and movie tickets.

And when people buy fewer products, companies make less money. This means that corporate earnings fall. And since stocks are priced based on future earnings expectations, high inflation leads to lower stock prices.

The dynamic and the Federal Reserve's response to it are the key reasons why the S&P 500 had one of its worst years ever in 2022:

But just like rising inflation caused stocks to crash last year, expectations of lower inflation is causing stocks to rally in 2023.

Same As It Ever Was

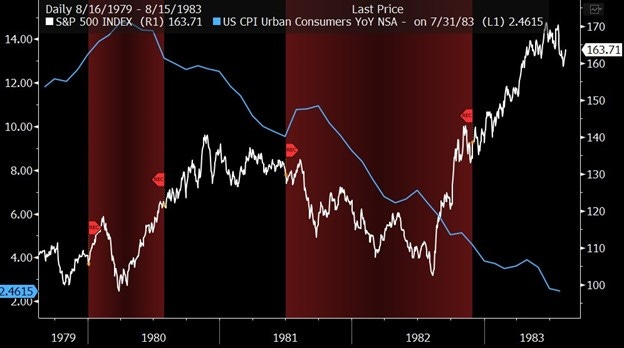

I wrote back in October that stocks would bottom when inflation peaked.

But I didn’t pull that prediction out of thin air; the S&P 500 (white line) hit bottom in the 1970s after inflation (blue line) peaked during the inflationary bear market from 1970-1979:

Similarly, we saw inflation peak at 9.1% in June and steadily decline since:

Not coincidentally, US stocks were within 1% of their lowest point of the year when inflation peaked in June 2022:

Because inflation is falling in an orderly fashion, the market now expects inflation to keep falling and even hit 4% in 2023:

The stock market is priced based on expectations, and most investors expect inflation to continue falling in 2023.

But what if those investors are wrong…

Going Against the Inflation Narrative

Every month, the Federal Reserve releases its Consumer Price Index (CPI) report.

This has loads of data on changes in consumer prices in the US. But the number everybody watches is the year-over-year change in the CPI, also known as the inflation rate.

The next CPI release is on Tuesday, February 14th…

…and since everyone believes inflation will keep falling in an orderly fashion, the biggest risk for stocks right now is that the inflation rate comes in higher than the 6.2% investors expect.

Or worse, a second surge in inflation, which happened twice in the 1970s:

So what will drive inflation higher? Logic dictates it will come from a familiar source: China.

China’s Reopening is Inflationary

China’s reopening from its COVID lockdowns has the potential to spur a new round of inflation in the US.

The pandemic caused widespread disruptions to global supply chains, including those between China and the US.

China’s reopening will increase demand for the goods and services traded between the two countries. That will put upward pressure on prices, particularly for goods and services that are in high demand and have limited supply like oil, metals, and agricultural products.

An increase in demand from China as its economy reopens could cause prices for these commodities to rise. And since commodity prices feed into many of the components that make up the CPI…

…higher commodity prices could translate to higher inflation in the US.

Hope For the Best, Plan for the Worst

My goal with this newsletter is to help you see around the corner of global financial markets.

China’s reopening may have little impact on US inflation. But what I look out for are the risks that nobody is factoring in.

And when everyone is thinking one way – like inflation will keep falling – that means the move to the downside will be violent if the consensus is wrong.

And while I’m still nearly fully invested in the market…

…I always plan for the worst but hope for the best.

And I’ll help you do the same.

Stay safe out there,

Robert