You Should Not Sit in Cash

Cash is trash even at 5% yields...

Before we get started, I want to welcome the +22 subscribers who signed up for the Let’s Analyze newsletter in the last week! If you want to join our community, make sure to sign up here:

Everyone reading this wants to make money.

You wouldn’t subscribe to an investment newsletter like this if you had any other objective.

But one mistake I keep seeing people make is they hold far too much cash.

Part of me understands the temptation to hold cash right now, as you can get over 5% risk-free in a money market fund right now.

Holding a small percentage of your portfolio - usually between 5%-10% - is fine at any time. But there are a lot of people’s largest holding is cash, including this commenter from my latest video:

And they’re not alone; US households currently have over $18 trillion in cash on the sidelines:

Now everyone has different investing goals and risk tolerances. I fault nobody for wanting to “play it safe.”

But if you’re trying to build wealth, sitting in cash can really set you back over the long-term.

Not So Safe After All

The 2022 bear market left many “cash holders” vindicated.

While everything from stocks to bonds to crypto was getting taken to the woodshed, those who were sitting in cash had a great time.

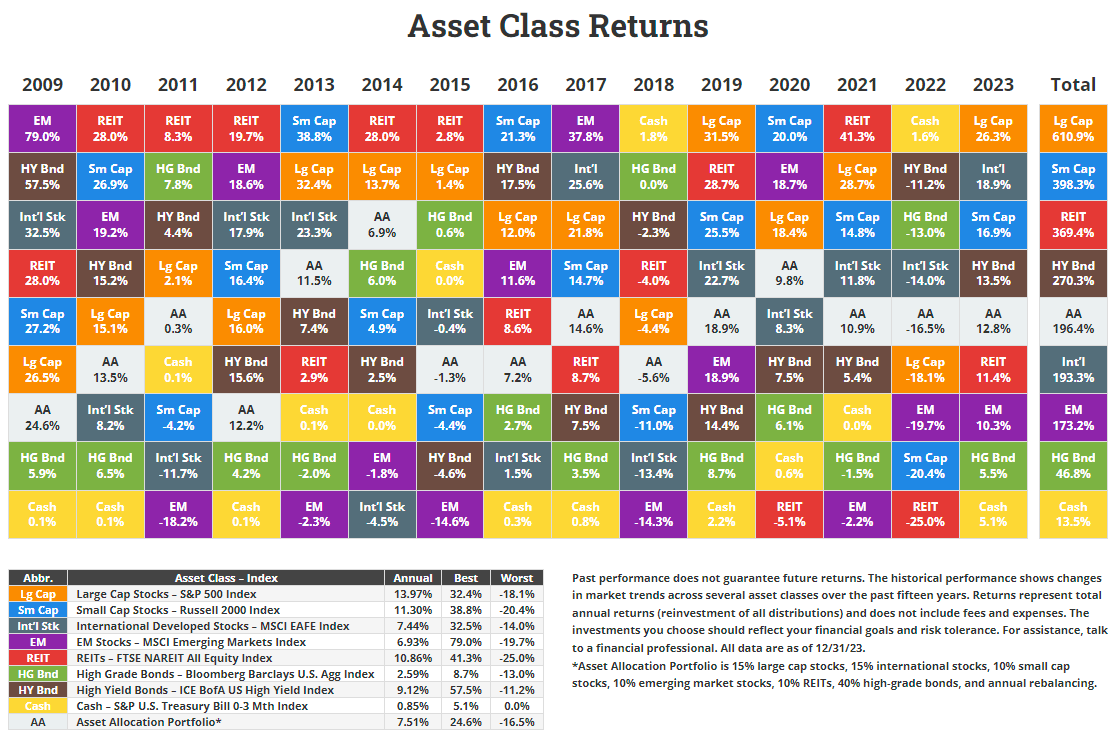

In fact, despite the highest inflation in 40 years, cash was the best performing asset classes in 2022:

But as anyone who reads these newsletters already knows, bear markets are the exception rather than the rule.

A study by NYU Stern School of Business showed that from 1926 to 2022, the U.S. stock market had positive annual returns in approximately 76% of the years, indicating a general upward trajectory.

That means every year US stocks have a down year, stocks rise for three years.

Going one step further, bear markets are historically much shorter than bull markets.

The average bull market lasts 991 days compared to 289 for bear markets. That means bull markets last nearly three-times longer than bear markets.

And whether it’s the Great Depression, World War II, 9/11, or COVID-19, the S&P 500 has always recovered to make new all-time highs. This is a core reason why I hold a large percentage of my portfolio in S&P 500 ETFs.

So while the “cash holders” had a good year in 2022, they miss out on tons of upside over the long-term.

And there’s plenty of data to back that up.

The Cost of Missing Out

When you're sitting in cash, you're not just playing it safe; you're potentially missing out on significant growth opportunities.

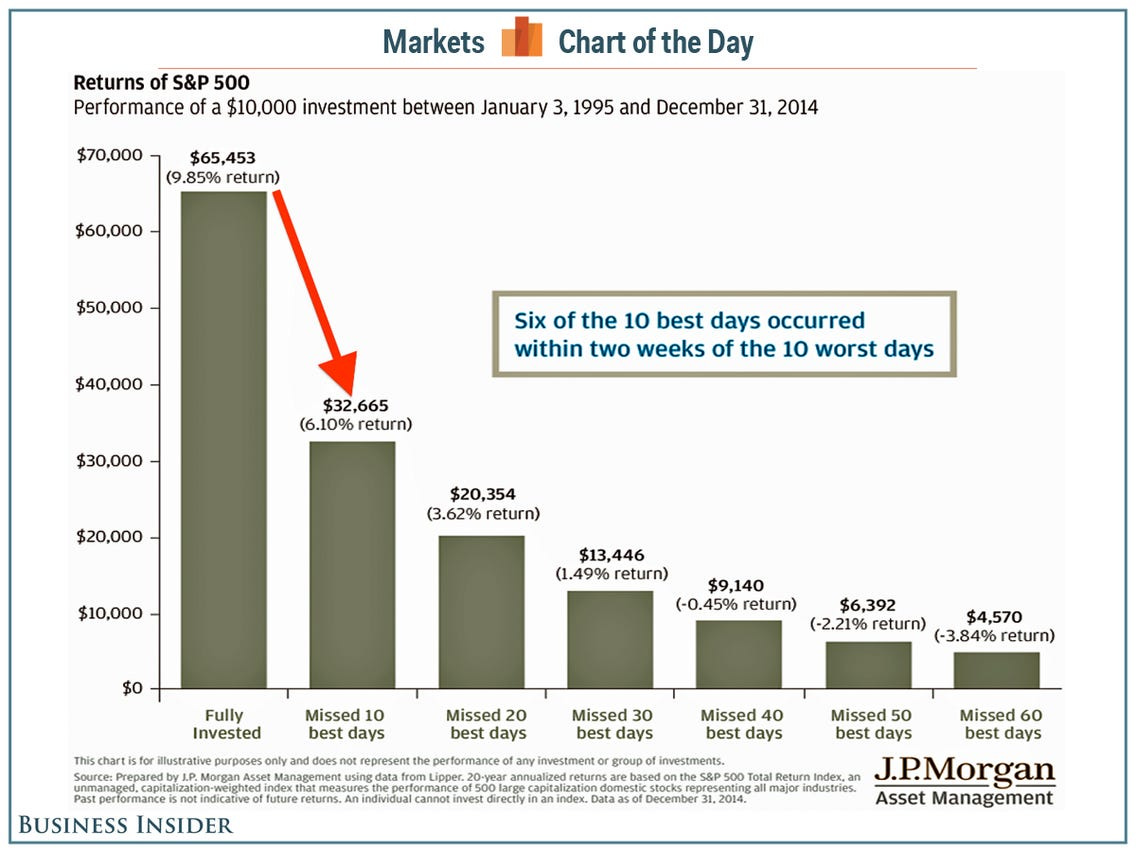

According to a study by J.P. Morgan Asset Management, if an investor missed the ten best days in the stock market over the last 20 years by holding an all-cash portfolio, their returns would be -50% lower than if they had remained fully invested in stocks.

Additionally, cash doesn't keep up with inflation over time.

The Consumer Price Index (CPI), which measures inflation, has historically increased by about 2-3% per year on average. This means that if your cash isn't growing at least at the rate of inflation, you're effectively losing purchasing power.

While that is not a problem at present with money market funds yielding 5%, the Federal Reserve is at the beginning of a rate cut cycle.

So don’t expect this paradigm to last much longer.

Striking the Right Balance

While it's prudent to keep some cash for emergencies and short-term needs, over-allocating to cash can be detrimental to your long-term financial goals.

The key is to find the right balance that aligns with your risk tolerance, investment horizon, and financial objectives.

Diversifying your portfolio across different asset classes, including stocks, bonds, crypto, and other investments, can help mitigate risk while providing opportunities for growth.

For me personally, I currently hold 8% of my portfolio in a money market account yielding 5.5% (you can see all my full portfolio in my premium newsletter here):

In the end, the goal is to ensure your money is working for you, keeping pace with inflation, and capitalizing on the long-term growth potential of the markets.

Remember, investing is about time in the market, not timing the market.

So, think twice before sitting on the sidelines with too much cash - the long-term cost might be higher than you realize.

Stay safe out there,

Robert