The Only Way to Beat the Market

It’s not as easy as it sounds…

Before we get started, I want to welcome the +78 subscribers who signed up for the Let’s Analyze newsletter in the last week! If you want to join our community, make sure to sign up here:

One of the largest banks in the US blew up this week.

Silicon Valley Bank (SIVB) – the former financier of some of the world’s premier tech companies – collapsed on Friday.

The reason for its downfall is interesting: they bought long-term US government bonds from 2019 to 2021. And when rates surged in 2022, the value of the bonds fell dramatically meaning there were no longer liquid assets backing deposits.

This left the company with a $2 billion hole on its books. And when word got out, SIVB experienced an old-fashioned bank run…

…which caused the US government to step in and take over the bank.

But there’s a lesson in here that will help you beat the market over the long-term.

And that lesson is you need to think different.

Following the Crowd

It’s hard to blame the bank’s risk management team for buying US government bonds.

After all, they had a huge influx of deposits from the tech bull run from 2018-2021…

…which caused their deposit base to balloon. The bank’s risk management team needed to put that cash somewhere. So they parked a lot of the cash in “risk-free” government bonds.

At the time, the US bond market had been in a 40 year-long bull market…

…which lulled SIVB and many others into a false sense of security.

That was until all hell broke loose in 2022.

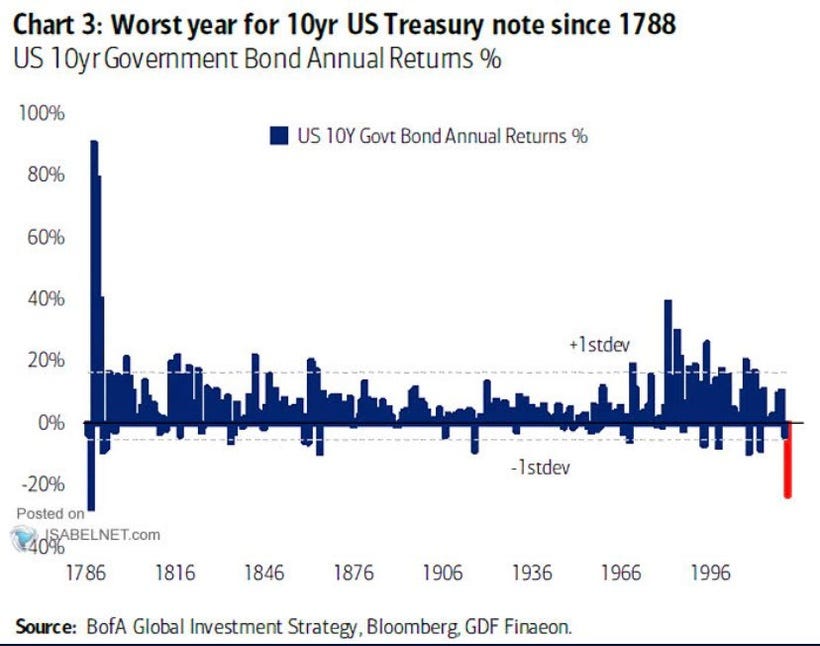

The Worst Year for Bonds Since 1788

Most retail investors only noticed that stocks and crypto had a tough 2022.

This makes sense as most retail investor completely ignore bonds.

But bonds had a famously tough 2022. In fact, it was the worst year for US government bonds since 1788:

Bonds had such a bad year that they actually lost more money than stocks…

…which had never happened in a bear market before. This makes sense as US government bonds are historically considered “risk-free” assets that move inversely to stocks.

Going one step further, it was widely believed that bonds would always fall less than stocks in a bear market. This is the exact concept SIVB’s risk management team followed, which led to their demise after the value of their government bonds collapsed when rates skyrocketed.

All of this could have been avoided if the bank hadn’t fallen under the spell of consensus.

The Dirtiest Word in Investing

In the investing world, following the “consensus” means you’re making investment decisions based on the prevailing opinions of the majority of analysts and investors.

Following the consensus can be a useful approach because it takes into account the collective wisdom and insights of a broad range of investors and analysts.

For instance, one consensus opinion I hold is that the S&P 500 will continue to rise over the long-term.

However, it's important to remember that the consensus is not always correct, and following it blindly can lead to missed opportunities or poor investment decisions.

And if you want to beat the market, you must hold at least some out-of-consensus opinions.

The Current Market Consensus

To come up with an out-of-consensus opinion, it’s helpful to determine what is currently consensus.

I typically look at the futures market to see what is in consensus. For instance, the futures market is telling us there’s a 70% chance the Federal Reserve hikes interest rates 0.50% at their next meeting.

The consensus also expects inflation to be back to 2% by the end of 2023…

…and that a recession is coming in the next six months:

Lastly, the futures market also tells us that investors expect interest rate cuts to begin at the end of 2023:

So which of these do I not agree with? You should be familiar with a few…

Going Against the Grain

Back in January, I laid out five market predictions for 2023.

A few of these fell under the market’s consensus at the time. That included the US falling into a recession in 2023 and the unemployment rate climbing above 5%.

But that’s where my consensus opinions ended. For instance, I still expect US government bonds to be the best performing asset in 2023…

…which has been pretty spot on so far. I also expected the S&P 500 to fall an additional 15% this year.

But considering the latest Silicon Valley Bank news, I’m not so sure about the latter.

My Latest Out-of-Consensus Idea

If there’s one thing the Federal Reserve doesn’t want it’s financial instability.

And with the second largest bank failure in history happening last week, they might need to stop raising rates as quickly as expected.

While it seems strange, the failure of Silicon Valley Bank may actually be good for stocks because the Fed will be forced to pullback on interest rate hikes.

They say when the Fed raises rates things, “tend to break.” Well, it looks like the central bank’s policy just broke the 13th largest bank in the US. And the last thing the Fed wants is a banking crisis.

And while this isn’t a consensus opinion yet, it may be before you know it.

Stay safe out there,

Robert