The Largest Position in My Portfolio

Investing is all about survival...

Before we get started, I want to welcome the +27 subscribers who signed up for the Let’s Analyze newsletter in the last week! If you want to join our community, make sure to sign up here:

I’ve invested through multiple market cycles.

That includes three bull markets, three bear markets, and two cryptocurrency crashes.

Despite these massive pullbacks, my portfolio has always bounced back to make new all-time highs.

But the reason I’ve survived and thrived so long in this business is due to my portfolio structure…

…and if you want to survive in investing, I highly recommend you follow my lead.

Most Investors Take On Too Much Risk

I asked my 120,000 Instagram followers what their largest position is.

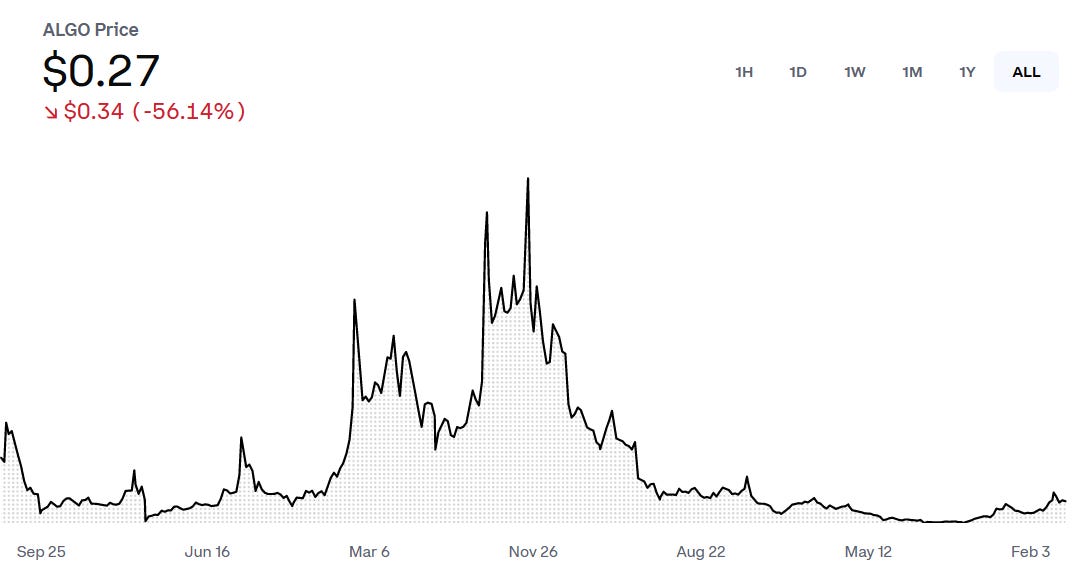

And some of the answers were a bit concerning. One follow said he had 50% of his portfolio in cryptocurrency Algorand (ALGO).

Another said the defunct video game retailer and meme stock Gamestop (GME) was his largest position:

While another said real estate website Zillow (Z) was their biggest holding:

While any of these investors could be right and make money on these positions, it is a bad idea to hold any of these as your largest position.

Because while many are trying to “get rich quick” by invesing in high-risk assets like cryptocurrencies, meme stocks, and high-growth stocks, they’re forgetting the #1 rule in investing.

Investing is About Survival

Everyone reading this probably knows I’m far from a “conservative” investor.

I take plenty of calculated risks with my portfolio in high-risk assets like high-growth stocks and crypto. In fact, I even wrote a book for one of the largest publishers in the US on investing in high-risk, high reward assets.

But the key word here is calculated. I invest in high-risk assets in a way that if I’m wrong, I won’t blow up my portfolio. And when a high-risk position - like Algorand, GameStop, or Zillow - is your largest position, you are not taking a calculated risk… you’re gambling.

Because when it comes to investing, your goal should be to survive to the next cycle.

That's precisely why the cornerstone of my investment philosophy isn't about chasing the next hot tip or getting swept up in the frenzy of the latest market craze.

It's about ensuring the longevity and resilience of my portfolio through thick and thin.

Keep Time On Your Side

The ability to endure and maintain a long-term perspective is what separates successful investors from the rest.

Because it’s only the long-term investor that reaches the point where their portfolio compounds.

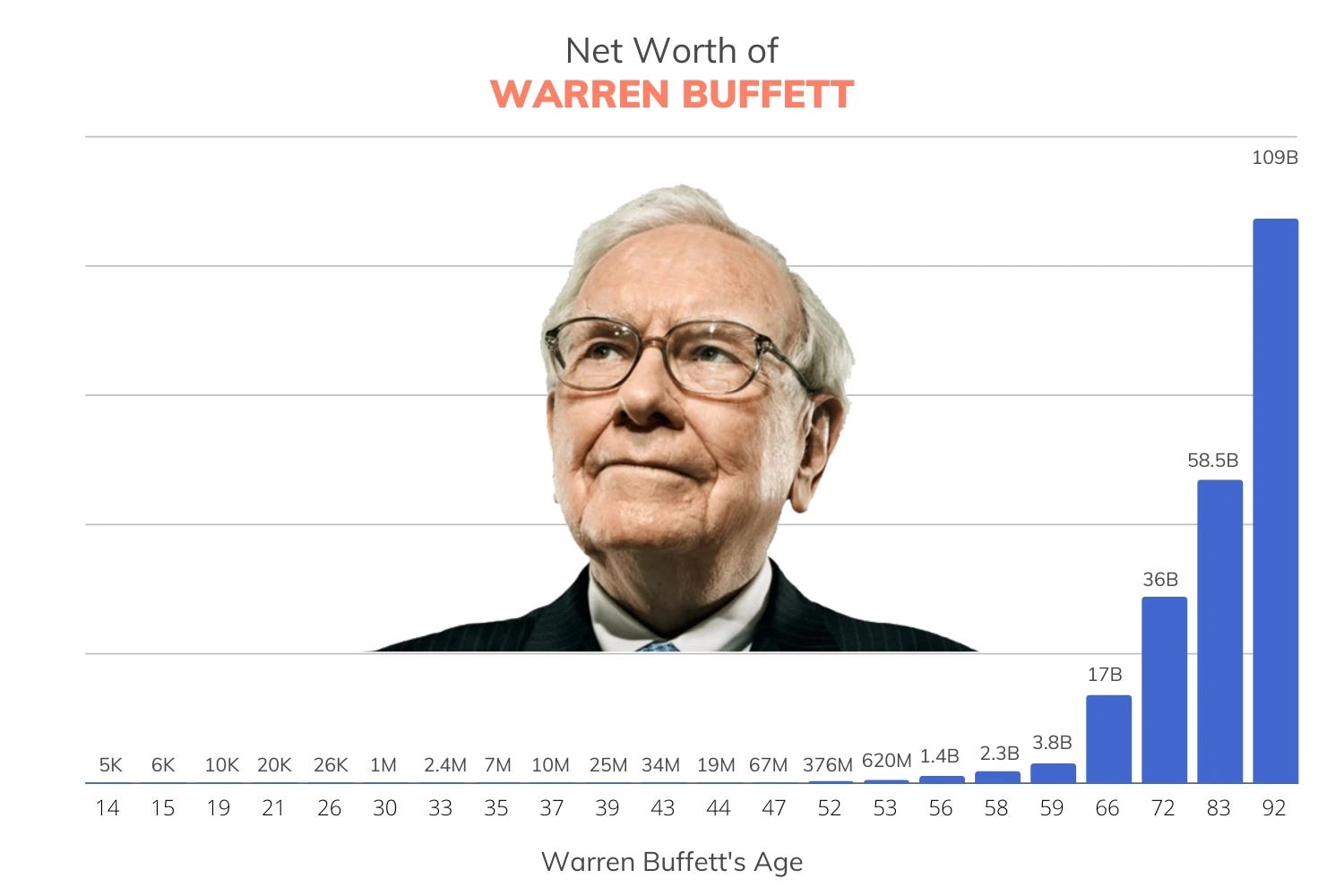

Take Warren Buffett, for example. Most know Buffett as one of the greatest investors of all-time. But what's less commonly understood is that the bulk of Buffett's wealth wasn't amassed in his early years of investing.

Rather, it was generated in the last two decades, a period during which his portfolio began to compound exponentially.

This incredible growth phase occurred not because he made radically different or riskier investments. Instead, it’s because he adhered to his principles of value investing, patience, and compounding returns over the long haul.

Buffett's journey underscores a vital lesson for all investors: the most significant gains often come not from chasing the latest market trends or betting it all on high-flying stocks.

Instead, it comes from the steady, relentless accumulation of wealth through sound investments and the magic of compounding over time.

Compounding Is Your Ticket to Wealth

Imagine you save $10 and it grows by $1 in a year because of interest.

Now, you have $11. Next year, you don't just earn interest on the original $10, but on the $11 you have now. So, if you get another $1 in interest, you have $12.

This keeps happening year after year. Your money grows faster over time because you’re earning interest not just on your original amount, but also on the interest that keeps adding up. It’s like a snowball rolling downhill, getting bigger as it picks up more snow.

That’s how compound interest makes your money grow expontentially.

But to get to the point where your wealth begins to compound, you need to survive.

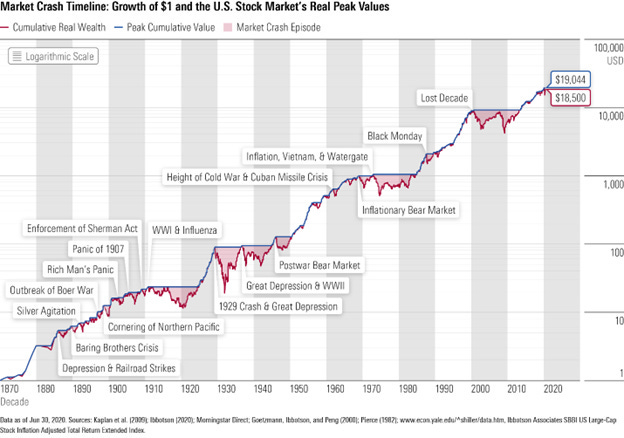

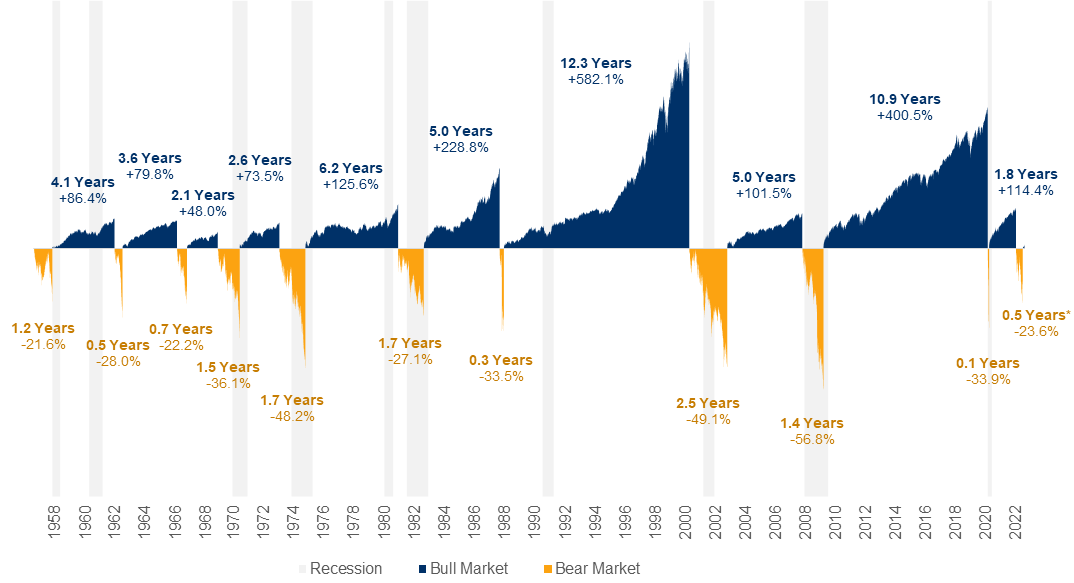

The goal is to hold investments that you know for near certainty they will bounce back… even after bear markets and crashes. As the charts at the outset show, there’s no guarantree cryptocurrencies, meme stocks, or high-growth stocks will ever bounce back after a crash.

But there’s one investment that will with near certainty.

My #1 Portfolio Position

My largest portfolio position hasn’t changed much in the last decade.

And there’s good reason for that. While I’ve only held this position for about 10 years (and add to it monthly), over the long-term it has recovered to make new all-time highs after:

The Great Depression

World War II

Vietnam War

9/11

Global Financial Crisis

COVID-19 Pandemic

And more recently, this same investment - the SPDR S&P 500 ETF (SPY) - recovered from The Great Inflation and subsequent bear market in 2022 to hit a new all-time high.

There are a few reasons investors of all stripes should hold index funds that track the S&P 500 like the SPDR S&P 500 ETF (SPY).

These ETFs are the bedrock of any investors’ portfolio, as they mimic the performance of 500 large publicly traded companies in the United States…

…giving investors diversification amongst many sectors and investing trends.

But the top reason to hold S&P 500 ETFs are the long-term gains. Over the last 90 years, the S&P 500 has delivered average annual gains of 10%…

…with the index delivering positive returns in 73% of those years.

And I don’t expect the next 90 years to be much different.

Work Smarter, Not Harder

Holding index funds like the SPDR S&P 500 ETF (SPY) allows me to take bigger risks elsewhere in the markets.

While past performance is not indicative of future results, it’s nearly guaranteed that the S&P 500 will deliver consistent gains over the long-term.

Holding a relatively low-risk holding like the SPDR S&P 500 ETF (SPY) means I can take on higher risk positions - like crypto, high-growth stocks, and private deals - in my portfolio (you can see my full portfolio here).

And while the S&P 500 finishes in positive territory nearly three-quarters of all years, there will be down years (like 2022). But it’s important to remember bear markets like last year are rare.

On average, bear markets happen every 3.5 years. They also tend to last, on average, for 289 days or roughly 10 months. That’s commpared to 991 days - or nearly three years - for bull markets.

And since gains during bull markets far outweigh losses during bear markets…

…it pays to be a long-term bull.

Holding index funds like the SPDR S&P 500 ETF (SPY) is the easiest way to profit from this historical trend. That’s a key reason the ETF accounts for roughly 20% of my portfolio.

And if I were you, I’d follow my lead.

Stay safe out there,

Robert