It Pays to Avoid This Investing Mistake

Bears sound smart but bulls make money…

Before we get started, I want to welcome the +43 subscribers who signed up for the Let’s Analyze newsletter in the last week! If you want to join our community, make sure to sign up here:

A new bull market officially started this week.

Since the October lows, the S&P 500 has risen 20%. This meets the technical definition of a new bull market.

Yet if you’ve been watching CNBC or scrolling on Twitter, you might think a market crash is imminent…

…which means now is a good time to debunk a few of the most common “threats” to this rally.

A Mountain Out of a Mole Hill

Financial media has a bias towards being “bearish” or pessimistic about the market.

The reason is simple: fear sells. A CNBC anchor telling their audience the worst is over for stocks doesn’t generate as many clicks as saying the “end is nigh.”

The latest bearish talking point is the US is going to default on its debt. You have people like former President Trump actively endorsing a default…

…with others opining over how a default would cripple the US economy:

Yes, it’s true that a US debt default would be bad for the US economy. But during my over a decade career as an investment analyst, I’ve seen multiple debt ceiling debates.

Spoiler alert: it always gets resolved at the 11th hour.

This was a sentiment echoed by Jim Bianco of Bianco Research on Bloomberg last week.

And while I expect the debt ceiling to once again be a nothingburger, there are other “bearish” talking points making the rounds…

The Recession That Never Was

I’ve written before that the yield curve inversion – a reliable recession signal – has been flashing red for over a year.

This along with the banking crisis have renewed calls for an imminent recession. But as the old saying goes, “economists have predicted nine of the last five recessions.”

For instance, in June 2022 nearly half of all economists surveyed by the Wall Street Journal expected a recession in the next 12 months:

But with unemployment at cycle lows, GDP growth positive, and consumer spending rising, there are few signs of an imminent recession (excluding the yield curve inversion).

While the debt ceiling and recessions are a common “bear” talking point as of late, there are a few market-centric ones I’d also like to dispel.

Every Stock I Don’t Own is A Bubble

A few weeks ago I wrote how analysts at JP Morgan said the rally in tech stocks was “by some measures the weakest ever.”

But the more I’ve dug into this, the less I agree. It is true that “mega cap” technology stocks like Microsoft (MSFT), Apple (AAPL), and Amazon (AMZN) - along with optimism over AI - have driven much of the market’s gains in 2023:

But that doesn’t tell the whole story. It is true that Apple and Microsoft – which account for 25% of the Nasdaq’s weighting – have driven much of the index’s rise this year…

…which - on the surface - seems to imply only a few stocks are propping up the tech rally.

That sounds like a good theory until you see that the equal-weighted Nasdaq 100 is up 17% in the last year compared to 20% for the main Nasdaq index:

Explained even more simply, even when Apple and Microsoft’s gains are normalized the Nasdaq is still having a great year.

But I can already hear the bears in the comments saying these tech stocks are in a “bubble” due to optimism over AI.

I don’t totally disagree with this one. But from a purely valuation standpoint, the top AI stocks – other than NVIDIA Corp. (NVDA) – are not expensive compared to their five-year average valuation:

Clearly many of the “bad signs” for the market aren’t so bad when put into context. In fact, I’m seeing more “good signs” than “bad signs” as of late.

Three Reasons for Stock Market Optimism

I must admit I did not expect stocks to rally so well in 2023.

But with the onset of the Bank Term Funding Program (BTFP) and the Fed ending their rate hike campaign, I quickly pivoted to a more bullish posture…

…which is why my personal investing portfolio is near a one-year high (you can see all my positions and real-time trades here):

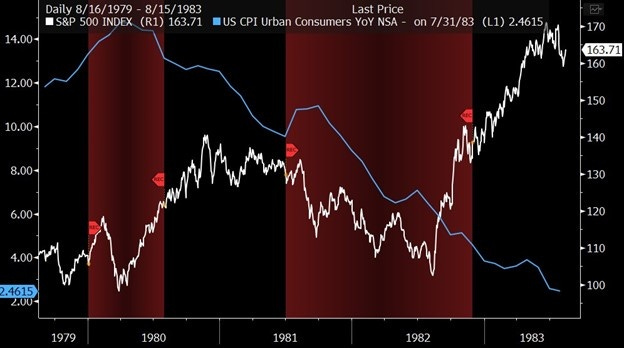

And there are a few reasons I remain optimistic. For one, it looks like inflation has officially peaked and the Federal Reserve will soon stop raising interest rates.

This “peak” in inflation was the catalyst for the market bottom during the 1970s bear market, and it looks like we’re following a similar trajectory in 2023:

Second, the S&P 500 has now gone seven months without hitting a new 52-week low. This has historically signaled the “lows” for the bear market are in.

In fact, of the 22 times this has happened since 1950, 19 of those times the S&P 500 was higher one-year later:

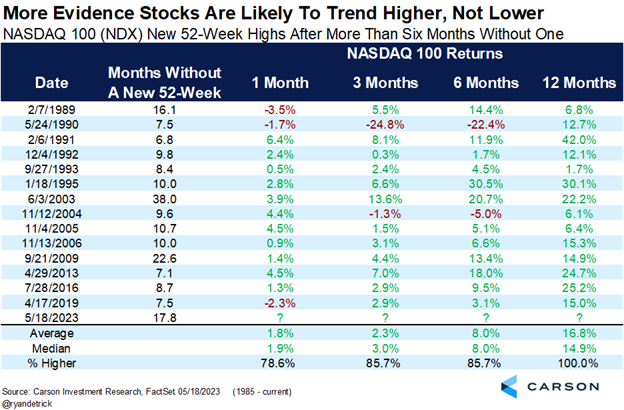

Lastly, the Nasdaq made a new 52-week high for the first time in 18 months last week.

And since every time the Nasdaq made a new high after more than six months without one the market was higher 100% of the time a year later…

…it’s a good time to stay optimistic on stocks.

Because while being bearish all the time is alluring, it’s one of the most common mistakes new investors fall into.

And as someone who’s been investing professionally for over a decade, I’m happy to put all the “doom and gloom” into perspective.

Stay safe out there,

Robert