Is it Too Late to Buy Tech Stocks?

Let history be your guide...

Before we get started, I want to welcome the +198 subscribers who signed up for the Let’s Analyze newsletter in the last week! If you want to join our community, make sure to sign up here:

My dad laughs when I tell him Alphabet (GOOGL) shares are cheap.

When he first started investing in the early 1980s, the largest company in the world by market cap was IBM Corp. (IBM).

At the time, the tech company had a valuation of $35 billion.

So when I tell him Alphabet just crossed a $1.7 trillion valuation, his hesitation makes sense.

But don’t let the gaudy figure throw you off…

…as the search giant - and other “expensive” tech stocks - have the earnings to backup these lofty valuation.

This Isn’t My First Rodeo

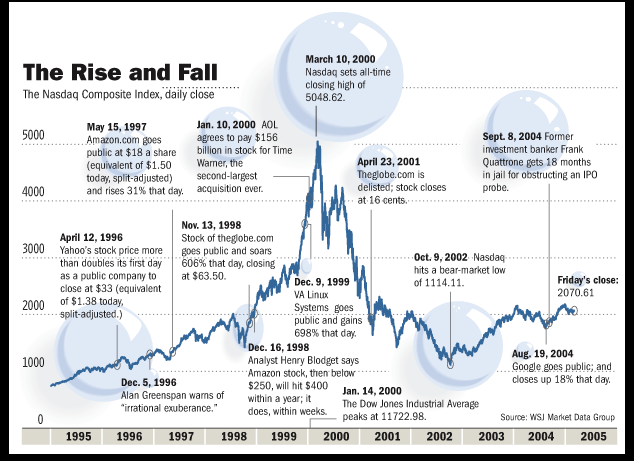

The Nasdaq 100 is up +115% in the last five years.

That’s spawned talk of a “Tech Bubble 2.0,” with many people—my family included—fearful of a Dot Com Bubble repeat:

But I’m not only holding on to my tech stocks, I’m adding to these positions every month.

I can hear you now: “But Robert, technology stocks are so expensive! We have to be in a bubble!”

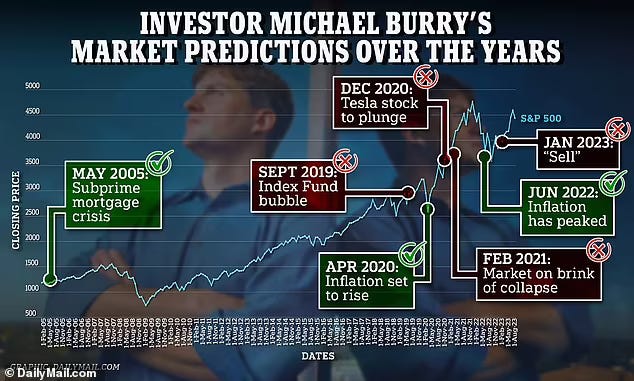

This type of thinking is common amongst new investors. Everyone wants to be the next Michael Burry and “call” the next crash.

But as we’ve said many times in this newsletter, “bears sound smart, but bulls make money.”

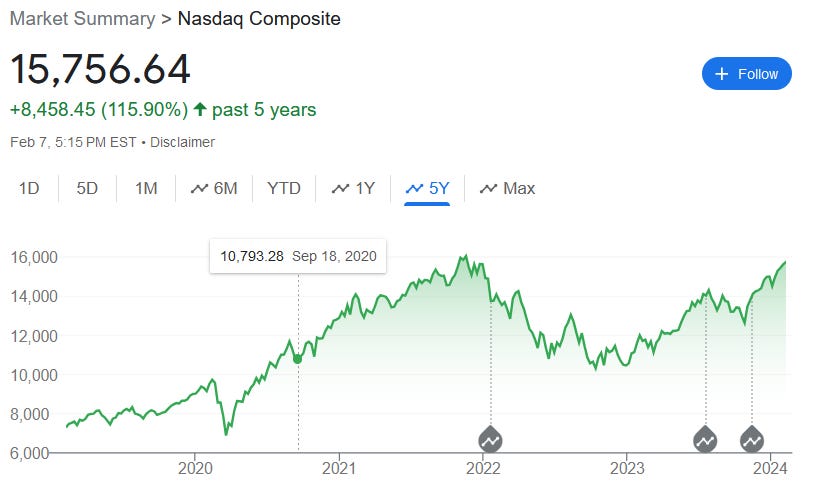

And I’ve stayed bullish on tech stocks for years. In fact, you can read this essay I published with Mauldin Economics from September 2020 titled “No Bubble Here” where I reiterated my call that tech stocks were not in a bubble (the Nasdaq is +46% since):

So how can I be so confident in this call yet again?

It all has to do with earnings.

Earnings Drive the Market

You may have heard people talk about “earnings” or “earnings reports” before.

When you hear someone saying this, they are referring to how much a company earned in total profit - the amount of money a business makes after subtracting all its expenses - in the latest quarter or year.

It's the difference between the revenue (the money a business earns from sales) and the costs (the money a business spends to produce and sell its products or services).

And growing these earnings consistently is key to making a stock go up.

Whether it’s the expectation of how much a stock will grow in the future or previous earnings performance, earnings and the “earnings multiple” – which we’ll get to in a future issue of this newsletter – are the keys to understanding what drives stock market returns.

Historical data supports the correlation between earnings and stock prices. Analysis conducted by Research Affiliates found a strong positive relationship between earnings growth and stock returns over the long term.

But don’t take their word for it; look at how expected earnings growth for the entire S&P 500 correlates with the S&P 500 itself:

Notice I’m saying “expected” earnings growth. Because when it comes to investing, you shouldn’t care as much about what a company did in the past. Instead, you want to focus on where the company is headed. And finding companies with the potential for explosive earnings growth is the best way to identify a stock that will potentially “go up.”

And when it comes to the “Magnificent 7” tech stocks, most have a favorable earnings growth outlook relative to their valuation.

Not All Tech Stocks are Created Equal

Six of the seven largest tech companies in the world reported earnings in the last two weeks.

And while many - like Alphabet - sport valuations in the trillions, many of these stocks are not as expensive as they appear.

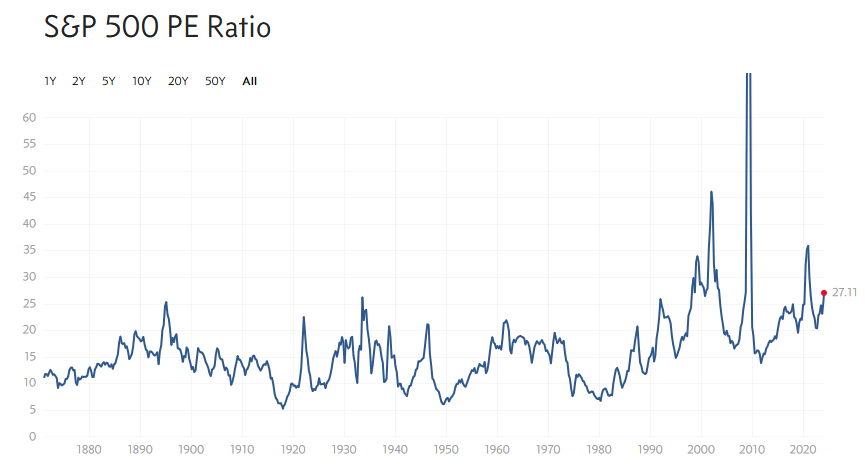

For instance, let’s look at Alphabet. While the stock trades at a $1.8 trillion valuation, they generated $5.81 in earnings per share in the last 12 months. That means the stock trades at a price-to-earnings multiple of only 18… which is far cheaper than the S&P 500 multiple of 27:

And over the next five years, the company is expected to grow these earnings by +19% per year. That means Alphabet shares - despite the $1.8 trillion valuation - are actually cheaper than if you simply bought the S&P 500.

When looking at the rest of the world’s largest tech companies, you see a similar pattern:

It’s true not all tech stocks have favorable valuations relative to their earnings growth - Alphabet (GOOGL) has the best ratio at present - which is why I don’t hold every mega cap tech stock (you can see which ones I hold here).

But on the whole, these are not the nosebleed valuations you might expect when you have multiple trillion dollar companies.

Keep Things in Perspective

Despite their eye-watering valuations, companies like Alphabet present a compelling case for investment when you consider their earnings growth relative to their price.

The key is to not get sidetracked by the sheer size of these numbers or swayed by the echo chamber predicting imminent doom for tech stocks.

Instead, focus on the fundamentals. Earnings growth remains a pivotal indicator of a company's health and its stock's potential for appreciation. And while many of the world’s largest companies trade at trillion dollar valuations, they are also generating billions in earnings. So it makes sense they have these sky-high valuations.

I know this stuff can be confusing. But that’s why I’m here to help explain to you in simple language why we’re seeing these unusual market dynamics.

Stay safe out there,

Robert